Did you ever have that awful feeling when you’ve reached the last few dollars of your paycheck yet you still have so many days left in the month?

If this sounds familiar, you are not alone. According to a new survey from CareerBuilder, nearly 8 out of 10 U.S. workers (78%) live paycheck-to-paycheck. What’s surprising is that one out of 10 workers making six figures say they live exactly the same!

We were just in the same boat and thought that there’d be no end to our paycheck-to-paycheck lifestyle. But I want to tell you that by being resourceful, learning how to spend wisely and using some money hacks, you can step out of the paycheck-to-paycheck cycle. Here are some effective tips!

I know what you are thinking. Budgeting sucks, right?

A lot of people think of budgeting as boring or no fun but it doesn't have to be that way. Budgeting should help you afford to have fun without harming your finances.

When you budget effectively, you may be able to find extra money you didn't know you had or stop spending money you don’t have. Think of it as your spending plan—it tells you how much you need to live, how much you should be spending, what you shouldn’t be spending on, and more!

A budget that works should have all of your expenses built into it so that you are not surprised of your taxes, insurance premiums and other expenses that don't occur regularly. In addition, it should help you deal with fluctuating bills.

If you want more ideas on how to create a realistic budget when you are living on a single income, check out this post.

You can simply list your expenses on a sheet of paper and budget your money accordingly or write them in an excel sheet. Another great tools to use for budgeting are apps like Digit or the cash envelope budgeting system.

These genius budgeting tricks will give you a better view of your finances to budget and better manage your money.

Pay Yourself First

Paying yourself first means saving before you do anything instead of saving what’s left over—that’s paying yourself last!

I understand this may not apply to everyone as not every person living paycheck-to-paycheck are just indiscriminately spending their income. Some are living paycheck-to-paycheck because they truly live on a bare-bone budget, but that’s when the next tips are important.

If your budget/ income allows it, sack a portion of your income towards savings. Let me tell you one thing though – don’t aim for the big dollars right away.

Even $100 a month will make you $1200 richer in one year. Start with a few dollars each paycheck and increase your savings rate as you figure out more ways to cut back from your budget. Build momentum. As you incrementally increase your savings, the more hyped up you’ll be with your progress.

I recommend having a separate account for your earnings and another savings. I receive my income in one account but I also have another account for my savings.

Bonus tip: automate your savings!

Automate your savings. It’s so much easier to save money this way as you don’t see the money being taken out of your accounts. Set up automated deposits every month to a separate savings account/s.

Live Below Your Means

I am sure you've heard of this a gazillion times but this tip is worth repeating because it can save you from going into debt spending more money you don't have. This has kept us debt-free as well even while relying on one small income for seven years!

Living below your means simply means not spending more than how much you earn. If the cost of the cost of your lifestyle is way too much for your income, cut back on your expenses and cut expensive habits. Give up a few other things like the gym membership you no longer use, cable ( we use Hulu to watch our favorite shows and save at least $40 a month!) and brand name products. Grow your own food, cook your own meals and eat out less frequently. Pocket the difference.

Living below your means takes some dedication but it is possible and it doesn't have to be difficult. There are so many ways you can save money or cut our spending every day.

One of the first things we did was cut our cable and switched to Hulu, or Amazon Prime. We've been saving over $900 per year on cable since! We also started meal planning, using shopping apps, and doing many things ourselves to save money. We've learned so many frugal living tips over the years that allowed us to live on one small income.

Ibotta– Ibotta pays you real cash money whenever, wherever you shop. Simply scan your grocery receipts using Ibotta and start earning cash backs. Receive up to $20 welcome bonus when you sign up here.

Update 2/5/2019- I have earned over $450 free money from Ibotta!

$5 Meal Plan –With the $5 meal plan, you will receive a weekly meal plan delivered straight to your mailbox.With each meal costing around $2 per person or $5 per family, the $5 Meal Plan is a really great tool to save money.

Your meal plan also comes with a grocery shopping list so you don’t overspend or buy extra ingredients you won’t eat. Try this service for free for two weeks!.

Ebates– Shop online with Ebates and earn cash back each time you shop online. Ebates has partnered with thousands of stores online, including Amazon so you'll no longer pay full price the next time you shop. Sign up here to receive free $10 from Ebates!

Swagbucks – It’s a cash back site, search engine and survey site in one. Earn points shopping online or by using the site as search engine, for watching videos, for answering surveys and more. Plus, they currently run a promotion offering free $10. Get it here.

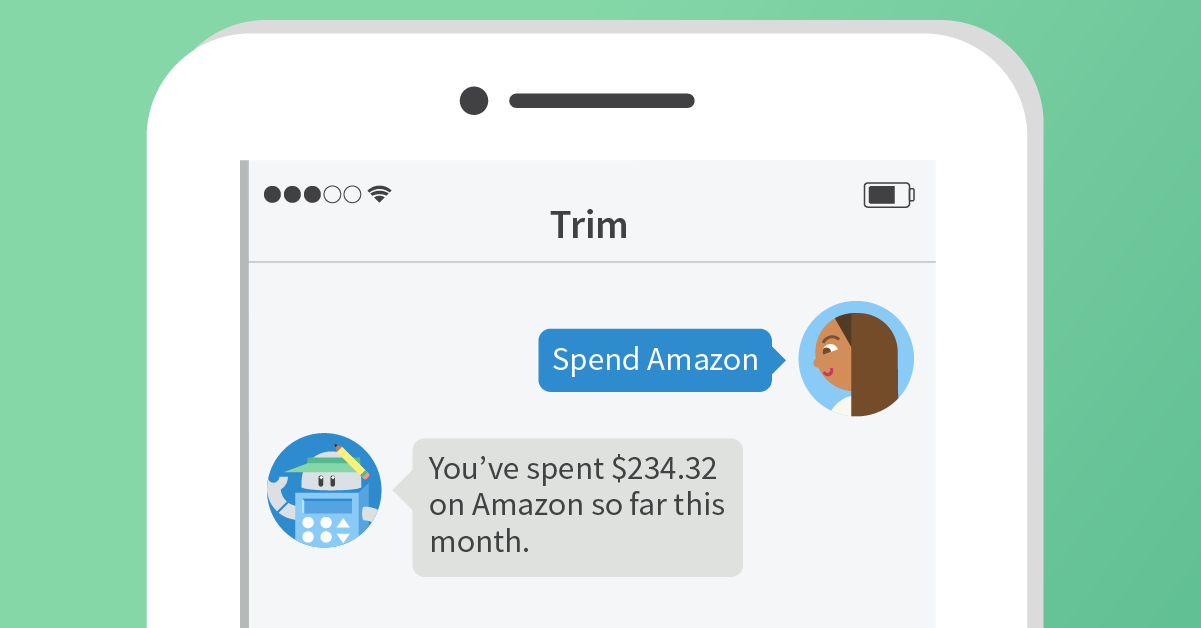

Trim Financial Manager - Trim will analyze your accounts to find recurring subscriptions and determine where you can save more money. You don't have to lift a finger. He can cancel subscriptions, negotiate your bill, find you better car insurance for you, and more. Trim has saved their users over $1,000,000 in the last month!

Increase your Income

If you’ve cut down your budget to bare bones and you’re still unable to make ends meet, then you obviously need to increase your income. You can only cut back to a certain extent. You definitely can’t take out food, transportation and housing from your budget, right? Fortunately, increasing your earnings is limited only by your imagination.

Getting a side hustle, second job or side gig (whichever way you want to call it) is a popular way to improve financial standing. Sure, you’re an accountant by day, but you can also be a consultant, blogger (start a blog for cheap here), pet sitter, dog walker, tutor, music teach and so on, on our free time.

On top of your regular income, you also get some extra money from your other jobs, which you can use to increase your savings and/or reduce debt.

If you are looking for great side hustle ideas, feel free to browse through this blog. I wrote a lot of posts about making money from home!

According to Nerd Wallet, in 2017, the average U.S. households carrying credit card debts owe over $15,000 and pay $904 in interest annually. That's a lot of money that only goes down the drain!

The best way to create a wiggle room in your budget is to tackle debt as soon as possible and get rid of it once and for all.

You might need to consolidate them or use Dave Ramsey’s Snowball Method to pay it off. It's definitely not an easy task but it is not impossible. Start by educating yourself, having a plan,and increasing your income. Stay committed!

These readings might help you stay focused and help you come up with strategies on slaying your debts (borrow these books or buy them—it’s a small investment that could help you!):

The mind is such a powerful thing. When it tells you “you need this fancy leather bag,” you’re bound to think that “yeah I probably need this.” There goes the gray line between “need” and “want” and before you know it, you’ve committed a very expensive mistake.

Catch yourself first before you take out your wallet or your purse. Spending money does give you certain bliss, but it’s short-lived. Instead of giving in to the temptation, give yourself the time to contemplate. Chances are, that purchase is just a want and would have covered your family’s two-week grocery.

Apart from curbing overspending, it also helps to be steadfast to your commitment in saving. Like they say, “saving money isn’t that hard. What’s hard is keeping money saved.” Don’t justify an expense to touch savings you’ve allocated for something else, for instance, your retirement or college fund. If the pull of a luxury is too much, think of how much time and effort you spent to save that money, only to go down the drain in a matter of seconds.

FINAL WORD

Everyone would probably say living paycheck-to-paycheck is tough, but nobody says you can’t get out of it. Combine all the steps above and you’d be making incredible progress soon enough. Also remember, to keep the gap between your expenses and income as wide as possible, and make sure to do something wise and meaningful to that gap.

I WOULD LOVE TO HEAR FROM YOU!

What tips do you have to stop living paycheck-to-paycheck?

Implementing a budget in my life was by far the most important thing I've ever done for my family's finances. I believe everyone should be in charge of their finances by using a budget and planning what to do with their money ahead of time.

Also, poor spending habits are the core of every poor bank account. Here are some dangerously poor habits that will keep people trapped in poverty: https://arielshanelle.com/habits-of-poor-people/

Thanks for sharing this wonderful post!

Jane

ThAnk you for stopping by and for sharing your wonderful posts as well.

Sharing is Caring

Help spread the word. You\'re awesome for doing it!

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.

Ariel Shanelle

Implementing a budget in my life was by far the most important thing I've ever done for my family's finances. I believe everyone should be in charge of their finances by using a budget and planning what to do with their money ahead of time.

You can read how having a budget changed my marriage here: https://arielshanelle.com/budget/

Also, poor spending habits are the core of every poor bank account. Here are some dangerously poor habits that will keep people trapped in poverty: https://arielshanelle.com/habits-of-poor-people/

Thanks for sharing this wonderful post!

Jane

ThAnk you for stopping by and for sharing your wonderful posts as well.