Hello mama!

Looking for a way to organize your family finances? The 70/20/10 budget is a great place to start.

Budgeting can feel intimidating. I used to think it meant strict rules, long spreadsheets, and tracking every single dollar-- but when I gave it a try, I realized it doesn’t have to be that way. It can be simple and freeing, helping me build a healthier relationship with money while keeping my spending aligned with what matters most to my family.

As moms, figuring out how to divide our income isn’t always easy—especially when surprise bills pop up, the kids need something last minute, or groceries end up costing more than expected. That’s why a simple system like the 70/20/10 budget is so helpful. They provide structure without making life feel more complicated.

What I love about the 70/20/10 method is how it helps you see the bigger picture. You can cover your needs, save for the future, and still have a little room to enjoy life.

There are many great budgeting methods you can try. I recommend exploring different options to find the one that best fits your family’s needs and financial situation.

In this post, I’m going to walk you through the 70/20/10 budget and show how it gives a simple, stress-free way to manage your money— no guessing, just a clear plan to guide your everyday choices.

What is the 70/20/10 Budget?

Table of Contents

The 70/20/10 budget is a budgeting method that helps you manage your after-tax income by dividing it into set percentages. Like other budgeting approaches, such as the 50/30/20 rule, it gives structure to your finances by focusing on daily expenses, savings, and personal growth or giving—making it easier to stay on top of your financial priorities each month.

Instead of tracking dozens of small expenses, you focus on three main categories:

- 70% for Needs & Wants – covers everyday living expenses, including both essentials and non-essentials

- 20% for Savings & Debt Paydown – includes building an emergency fund, saving for retirement, and making extra debt payments

- 10% for Giving and Personal Growth – set aside for charitable giving, tithing, donations, or personal development

This approach keeps your spending simple and organized, while still allowing you to cover essentials, plan for the future, and invest in yourself or others.

Focusing on these three key areas makes it easier to stay consistent with your budget and track your progress over time. Research shows that people with a household budget feel more in control and confident about their financial situation compared to those without one, highlighting the value of having a clear framework like the 70/20/10 budget.

Breaking Down Each Category

To make the 70/20/10 budget easier to follow, let’s take a closer look at the three categories and what each covers.

70% Needs & Wants

This part covers the costs of your day-to-day life—both what you need to live comfortably and a few things you enjoy. It’s where most of your money goes, so planning carefully here helps keep the rest of your budget on track.

Types of expenses that fit here:

- Housing and utilities: Rent or mortgage, electricity, water, internet

- Groceries and food: Supermarket shopping, coffee runs, occasional dining out

- Transportation: Gas, public transit, car maintenance, ride shares

- Lifestyle and small treats: Clothing, entertainment subscriptions, hobbies

Common Mistakes to Avoid in this Category

- Overspending on non-essentials – Buying trendy gadgets, fancy coffee, fun accessories, or items you don’t really need can add up fast. This can quietly push your 70% allocation over the limit, leaving less for savings and essential bills.

- Relying on convenience– Using services like grocery delivery, rideshares, or same-day shipping may save time but gradually drains your budget. A study found that ordering meals through delivery apps can cost about 79.5% more than picking up the same meal yourself, showing how convenience can add a noticeable extra cost to your monthly spending.

- Ignoring recurring small expenses – Small subscriptions or frequent app purchases may seem harmless, but they can snowball little by little and quietly eat into your budget, creating unexpected financial stress.

- Forgetting irregular expenses – Things like seasonal clothing, car maintenance, or school supplies can catch you off guard if not planned for. When that happens, it can gradually stretch your monthly spending and put extra pressure on other areas of your budget.

Tips for Staying Within 70%

- Prioritize essentials – Cover bills, groceries, and transportation before splurging on wants. This ensures that your basic needs are always met.

- Plan meals and groceries – Create a monthly grocery list to reduce last-minute takeout or impulse buys. Sticking to a plan keeps daily spending predictable.

- Automate bills – Automatic payments prevent late fees and reduce mental load. This keeps your finances on track and helps you stick to your budget without stress.

- Review and tidy up your finances – Regularly check your accounts, subscriptions, and spending patterns to spot leaks or unnecessary costs. Doing a financial “deep clean” helps you stay aware of where your money is going and keeps you in sync with your spending.

20% for Savings & Debt Paydown

This portion of your income is dedicated to building financial security and preparing for the future. It helps you handle unexpected expenses, reduce debt faster, and grow your long-term savings.

Types of expenses that fit here:

- Emergency fund: Money set aside for unexpected bills, such as car repairs or medical expenses.

- Debt paydown: Extra payments beyond minimum on credit cards, student loans, or personal loans.

- Retirement savings: Contributions to 401(k), IRA, or similar accounts.

Common Mistakes to Avoid in this Category

- Only paying minimum debt amounts – Putting just the minimum toward credit cards or loans keeps you in debt longer. This makes it harder to build an emergency fund or grow your savings steadily, slowing your overall financial progress.

- Neglecting an emergency fund – Skipping emergency savings leaves you vulnerable to unexpected expenses. Without it, even small setbacks like a car repair or urgent home maintenance can push you into new debt and financial stress.

- Using savings for non-emergencies – Dipping into your emergency fund or debt savings for everyday spending can derail your financial progress. Keeping these funds reserved ensures you’re prepared for unexpected bills and can steadily pay down debt.

- Delaying or splitting contributions inconsistently -- Frequently delaying or splitting your 20% between debt payoff and savings makes it more challenging to stay consistent with the plan. Inconsistent progress slows debt repayment and prevents your emergency fund and retirement savings from gaining momentum.

Tips for Staying Within 20%

- Tackle high-interest debt first – Focus extra payments on the highest-interest loans or credit cards. Paying these off faster reduces interest costs and frees up more money for savings.

- Keep a “rainy day” buffer – Before fully maxing out debt payments, make sure your emergency fund has 1-2 months of living expenses. This provides a cushion for unexpected costs while keeping you on track.

- Use separate accounts – Keep emergency funds, debt repayment, and retirement savings separate. This prevents accidental spending and makes it easier to track progress.

- Automate your savings and payments – Set up automatic transfers to your savings, debt, and retirement accounts so your 20% goes straight to your financial goals. Automation ensures consistency and reduces the risk of overspending.

10% For Giving & Personal Growth

This category focuses on allocating a portion of your income to meaningful contributions and personal development. It’s about supporting causes you care about, investing in yourself, and enriching your life in ways that truly matter.

Types of expenses that fit here:

- Charity of tithing: Donations to non-profits, religious contributions, or community support

- Learning and self-improvement: Online classes, books, professional courses, or mentorship programs

- Hobbies and personal enrichment: Activities that expand your mind or skills, such as art, music, or fitness classes

Common Mistakes to Avoid in this Category

- Overcommitting financially – If you donate more than you can afford, it can put pressure on the rest of your budget. Giving is meaningful, but it should never compromise your financial stability.

- Not planning for occasional big expenses – One-time costs like seasonal donations, annual workshops, or special events can strain your budget if you don’t prepare for them. Unexpected expenses may force you to dip into funds meant for other priorities.

- Skipping free learning or enrichment resources – If you skip free courses, workshops, or community programs, you may end up spending unnecessarily on paid options. Overpaying for things you could get for free can eat into what you’ve allocated for other financial commitments.

- Failing to set clear priorities – Treating your 10% as flexible “fun money” rather than purposeful giving can reduce the real value of your contributions. Without clear priorities, money meant for meaningful growth or giving often gets spent on less important things.

Tips for Staying Within 10%

- Set a realistic giving and growth budget – Decide on amounts you can comfortably allocate to donations, learning, and personal enrichment. This keeps your contributions meaningful without putting a strain on the rest of your finances.

- Prepare for irregular opportunities – Even within your 10%, occasional events like seasonal donations, special workshops, or one-time mentorship programs can come up. Planning ahead ensures you can participate without affecting other giving or growth activities.

- Use free or low-cost resources – Take advantage of free courses, community programs, library resources, or online tutorials. Using these options reduces unnecessary spending while still supporting your personal growth.

- Define your priorities clearly – Decide what giving or learning goals matter most to you before spending. Clear priorities help prevent your 10% from losing focus to casual or less meaningful purchases.

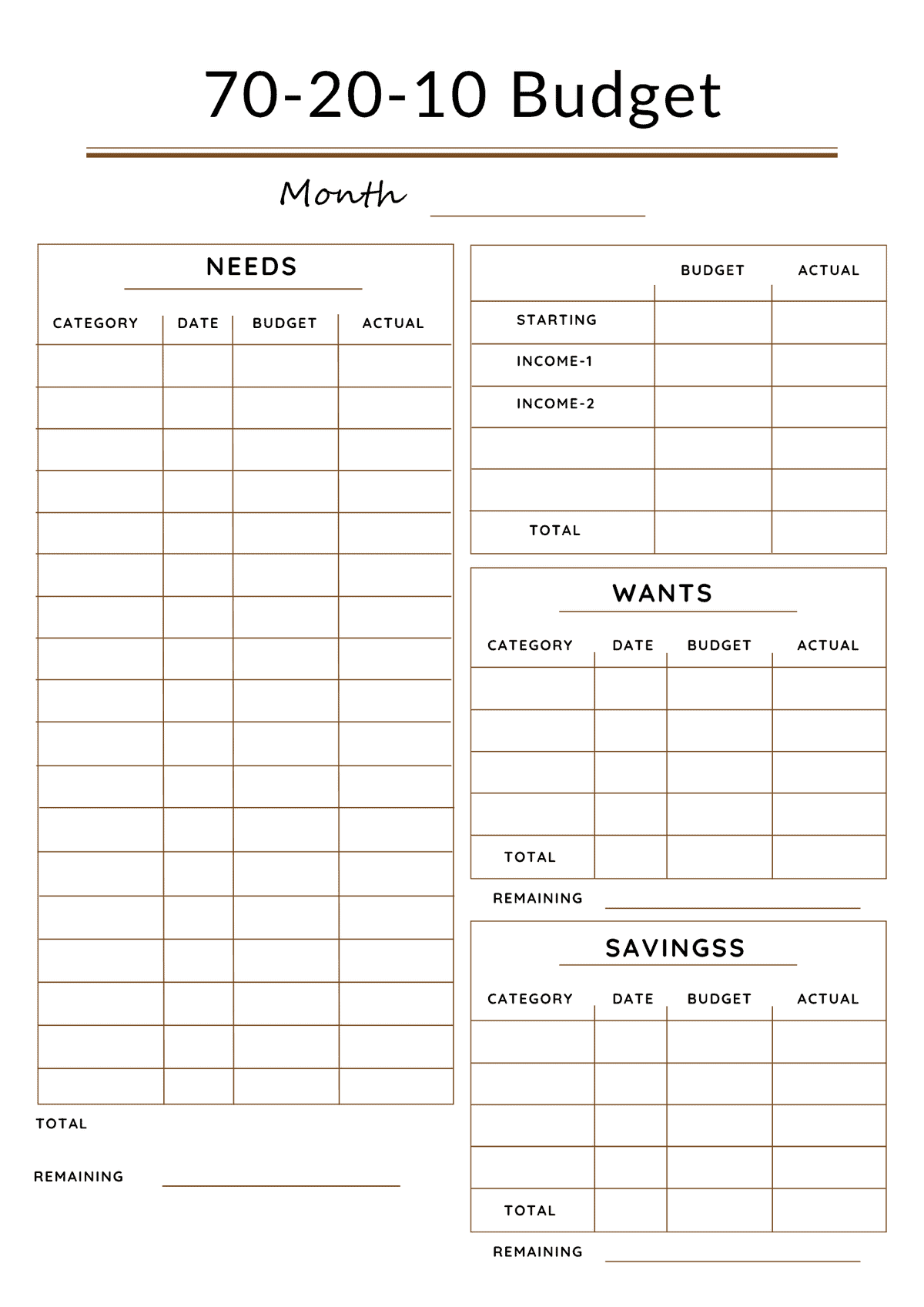

Sample Monthly Budget Using the 70/20/10 Method

Keeping your finances in check can feel overwhelming, but a simple plan makes it much easier to handle. If you want to give the 70/20/10 method a try, I’ve created two sample budgets based on different income levels. To start, here’s an example based on the average U.S. take-home pay.

Monthly Take-Home Income: $5,000

| Category | Expense | Amount | Why It Fits This Category |

| 70% Living Expenses ($3,500) | Rent/Mortgage | $1,500 | Housing is a basic necessity and anchors your monthly expenses |

| Utilities | $250 | Electricity, water, and gas are essential household services. | |

| Groceries | $400 | Food is a non-negotiable daily need | |

| Transportation | $300 | Commuting supports work and daily responsibilities | |

| Insurance | $350 | Protects your health, income, and property from financial risk | |

| Phone/Internet | $150 | Needed for communication, work, and school access | |

| Personal and Household Essentials | $200 | Includes essential items for daily living and home care | |

| Entertainment | $350 | Makes room for leisure and fun while keeping spending in check | |

| 20% Savings & Debt ($1,000) | Emergency Fund | $300 | Builds a safety net for unexpected expenses |

| Retirement Contributions | $400 | Ensures long-term financial security | |

| Extra Credit Card or Loan Payments | $300 | Helps pay off debt faster and eases financial pressure | |

| 10% Giving and Personal Growth ($500) | Charitable Giving/Tithes | $150 | Aligns spending with personal values |

| Donations | $100 | Supports meaningful causes and community needs | |

| Courses, Books, Skill Development | $250 | Improves knowledge and future earning potential |

Total : $5,000

If your income is below average, or your budget feels a bit tight, don’t worry—here’s how the 70/20/10 method can work for you.

Monthly Take-Home Income: $2,500

| Category | Expense | Amount |

| 70% Living Expenses ($1,750) | Rent/Mortgage | $750 |

| Utilities | $150 | |

| Groceries | $270 | |

| Transportation | $165 | |

| Insurance | $150 | |

| Phone/Internet | $100 | |

| Personal and Household Essentials | $115 | |

| Entertainment | $50 | |

| 20% Savings & Debt ($500) | Emergency Fund | $150 |

| Retirement Contributions | $100 | |

| Extra Credit Card or Loan Payments | $250 | |

| 10% Giving and Personal Growth ($250) | Charitable Giving/Tithes | $30 |

| Donations | $20 | |

| Courses, Books, Skill Development | $200 |

Total : $2,500

Pros and Cons of the 70/20/10 Method

Like any budgeting method, the 70/20/10 budget has its strengths and a few things worth keeping in mind. Understanding both can help you decide if it’s the right fit for your finances.

Pros of the 70/20/10 Method

1. Works Well for Steady Income

If your income is fairly predictable each month, this method clearly shows how your money should be allocated—covering essentials, building your savings, and reserving a portion for personal growth—without leaving you guessing.

Following it consistently makes handling unexpected bills or occasional treats easier, keeping your budget on track without stress. Over time, it quietly builds confidence and a steady sense of control, making managing your finances feel simpler and less stressful.

2. Keeps Your Priorities Balanced

For moms managing family needs alongside their finances, it’s easy to feel pulled in every direction. The 70/20/10 method offers a clear view of where your income goes—so nothing important is overlooked.

It shows how each part of your budget—day-to-day expenses, savings, debt repayment, and personal growth—works together, giving you the space to focus on what truly counts without letting any one area take over.

3. Straightforward and Easy to Follow

Keeping your budget simple makes it easier to actually follow. The 70/20/10 method breaks your income into just three main categories, so you don’t get bogged down tracking every little expense.

With a clear plan in place, you can create a routine that flows smoothly with your family’s daily life while still making progress toward your goals. It makes managing your money feel effortless, even when life gets busy.

Cons of the 70/20/10 Method

1. Can Feel Tight in High-Cost Areas

In cities or regions where everyday expenses are higher, the 70% allocation for essentials can be a little restrictive. For example, in places like Manhattan, the cost of living—including housing, groceries, and services—is more than double the U.S. national average, which makes fitting everything into that 70% much harder.

Without some wiggle room, the budget can feel tight rather than guiding. Fixed percentages do not always match the realities of living in higher-cost urban areas.

2. May Slow Repayment of Large Debt

The 20% allocation for savings and financial goals may not feel sufficient if you’re carrying significant high-interest debt. Progress can seem slow, especially when interests continue to add up each month.

The fixed percentage may limit how quickly you can reduce balances. For those with heavy debt, the structure can feel less aligned with their most urgent financial priority.

3. Less Flexible During Life Changes

Major life shifts—like a new job, relocation, or growing family—can quickly change financial priorities. A fixed percentage split may not reflect those new realities right away.

What once felt balanced can feel slightly out of sync with your current needs. If you stick to it too rigidly, the structure can end up more of a cage than a compass.

Tips for Making the 70/20/10 Budget Work in Real Life

The 70/20/10 budget is straightforward, but making it work in real life takes intention and consistency. Here are simple tips to help you put it into action and stick with it.

1. Be Intentional with Your Spending

If you’re not careful, little expenses can fly under the radar and quietly throw off your budget. To make the 70/20/10 plan work in real life, look for small ways to trim everyday costs-- cook at home instead of eating out, pause unused subscriptions, hunt for better deals on bills and groceries, and skip impulse purchases like daily coffee runs or last-minute online shopping.

Being mindful of these choices helps you keep essentials within 70% and ensures your savings and personal growth goals stay on track. This gives you more control over your finances and the freedom to focus on what truly matters.

2. Automate Your Savings

Saving works best when it’s built into your routine instead of relying on motivation. Setting up automatic transfers right after payday ensures your 20% for future goals and 10% for personal growth are moved before you even get the chance to spend it elsewhere.

In the U.S. retirement plans that automatically enroll employees see participation above 90%, compared to much lower rates when employees have to sign up on their own— showing that automation makes it much easier to follow through.

3. Keep an Eye on Your Expenses

If you let it, money can easily slip through the cracks—but a little weekly check-in keeps it in view without feeling overwhelming. You don’t need to track every dollar to stay on top of your 70/20/10 plan-- just a simple budgeting app, or a quick glance at your bank statements lets you see the bigger picture of what’s coming in and going out.

To make it even easier, I created a printable tracker you can peek at anytime, keeping your spending visible but under control-- so you can focus on your goals instead of micromanaging every cent. Simply print this budget planner below.

Looking for More Money or Budget Ideas?

Feel free to browse through the following!

Final Thoughts

The 70/20/10 budget isn’t magic—it won’t fix every financial challenge overnight, and it doesn’t promise perfection. What it does offer is a simple framework to organize your income into essentials, savings, and personal growth, helping you stay on track with your finance goals and giving you a sense of where your money flows.

You don’t need to track every tiny detail. Use the plan as a guide and check in on your progress regularly. Little by little, these steps add up—like laying one stone at a time to build a strong, steady foundation. With patience and consistency, budgeting becomes a tool to support the life you truly want, not just a list of numbers to manage.