Do you ever find yourself struggling to stick to your budget, even though you’ve planned everything out perfectly? Then, out of nowhere, an unexpected expense throws your entire plan off track.

Budgeting can feel overwhelming with so many things to juggle—groceries, savings, and the occasional extra expense. It’s easy to lose control and feel like you're not making progress.

If you're finding it tough to manage, the 50/30/20 rule could be the solution you need. I personally love this method because it’s simple, straightforward, and—most importantly—it works! It was the first budgeting approach I used when I was new to managing my finances, and it’s been a game-changer ever since.

In this post, I’ll walk you through how to create a budget using the 50/30/20 rule for average and low income.

What is the 50/30/20 rule?

Table of Contents

The 50/30/20 rule is basically a way to divide up your income into three neat little categories: needs, wants and savings.

In this budgeting approach, 50% of your income goes to your needs, 30% to your wants, and 20% should go straight into your savings account.

This rule was popularized by Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi, in their book “All Your Worth: The Ultimate Lifetime Money Plan.”

The Three Categories to Budget For in the 50/30/20 Budgeting Method

Needs (50%)

Have you ever thought about what exactly needs are? It might seem like a simple concept, but let’s dive a little deeper into it.

Needs are things you really have to have in order to survive and live a decent life. These things include a place to live, utilities like water and electricity, a car, healthcare, and childcare if you have children to take care of.

But here’s the thing – while these “needs” seem straightforward, everyone can have different ideas about what exactly counts as a need. Take a car, for example. Some people might see it as a need, especially if they live in a place with limited public transportation. Others might see it as a luxury if they can get around just fine without one.

The point is everyone’s needs are unique. It all depends on your personal situation and what you value most.

Wants (30%)

When we talk about wants, we are referring to things that we desire but don’t necessarily need to survive. They are often called non-essentials because you can live without them.

Think of wants as the things that make life more enjoyable and personal. For example, while you need food to survive, eating out at a fancy restaurant is a want. You could easily cook a meal at home for a fraction of the cost, but choosing to dine out at a restaurant is a want because it adds a level of luxury and convenience to your dining experience.

Other examples of wants could include buying designer clothing, going on vacations, and owning the latest technology gadgets.

Savings and debt (20%)

The breakdown of how you allocate that 20% will depend on your own personal situation. If you have high-interest debt, it may be wise to focus more on paying that down first before prioritizing savings.

On the other hand, if you don’t have much debt but want to build up your emergency fund, you might choose to put more towards savings.

It's important to regularly review your financial situation and adjust your savings and debt repayment plan as needed. Everyone’s financial situation is unique, so what works for someone else may not work for you. Take the time to evaluate your own finances and make a plan that fits your goals.

Why follow the 50/30/20 rule?

Budgeting can be overwhelming and complicated, but with the 50/30/20 rule, it can be much simpler and more manageable. Here’s why I recommend the 50/30/20 rule for those who are new to budgeting.

- It provides a simple and straightforward layout of how to divide your income. It gives you a clear picture of where your money is going each month. By sticking to these guidelines, you can avoid overspending in one area and falling short in another.

- It’s easier to understand and follow than other budgeting methods. It doesn’t require you to track every single expense. Instead of getting bogged down in the nitty-gritty details of every purchase, you can focus on the bigger picture and ensure that you’re meeting your financial goals.

- It allows you to prioritize your spending while still having some room for fun. Dedicating 30% of your income to wants might sound like a lot, but it’s actually a good way to make sure you’re still enjoying life while also being responsible with your money.

- It helps in reducing your debt. Every little bit counts when it comes to paying off debt. By setting aside a portion of your income towards debt repayment, you can gradually chip away at what you owe and work towards becoming debt-free.

- It tells you exactly how much you should save. Knowing exactly how much you should be saving each month gives you a concrete number to work towards. This way, you’ll have a little nest egg for any unexpected expenses that come your way.

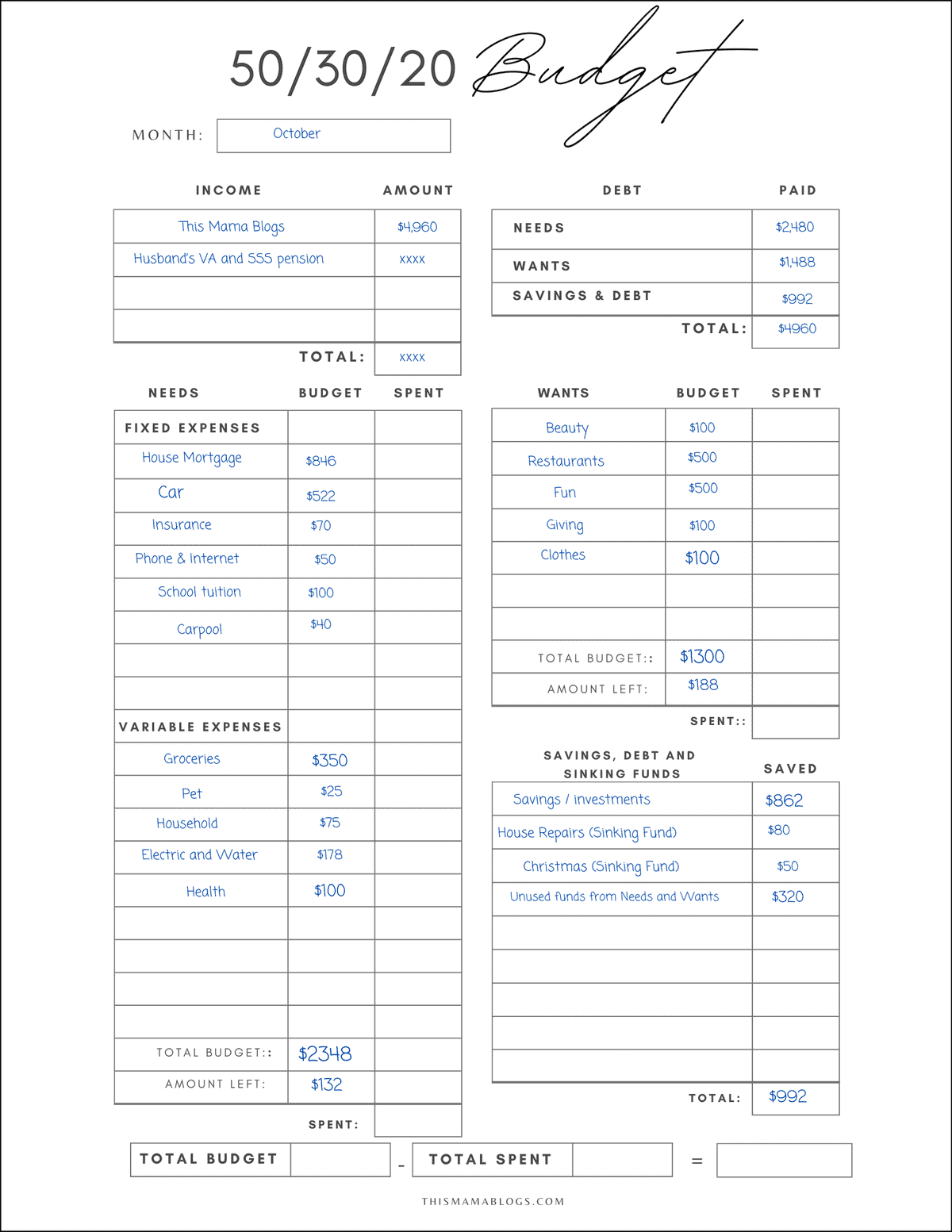

Sample Budget for Average Income

The average monthly income in the United States is approximately $4,960, though this figure can vary significantly depending on factors like your location and occupation. Areas with a higher cost of living often offer higher salaries to offset these expenses.

If you earn around $4,960 per month, you can effectively manage your finances using the 50/30/20 budgeting rule. Here's how you can break down your income:

- 50% for needs: $2,480 (e.g., housing, groceries, transportation)

- 30% for wants: $1,488 (e.g., dining out, entertainment, hobbies)

- 20% for savings and debt: $992 (e.g., emergency fund, retirement, loan payments)

To figure out how much money you need to allocate to each category, you’ll need to do a little math. Take your total income and multiply it by 50%, 30%, and 20%.

Low Income

In the United States, a low-income earner is typically defined as someone that earns less than the federal poverty line. This amount can vary depending on where you live and how many people are in your household.

However, on average, it hovers around $14,580 per year for a single person, and $30,000 for a family of four. If we break that down into monthly income, it comes out to around $1,215 per month for a single person and $2,500 for a family of four.

So, you’ve got a monthly income of $2,000, and you’re trying to figure out how to budget it wisely. Let’s divvy up that cash using the 50/30/20 rule. Here’s what your budget looks like.

- 50% for needs = $1,000

- 30% for wants = $600

- 20% for savings and debt = $400

How to Create a Realistic Budget Using the 50-30-20 Budget Approach

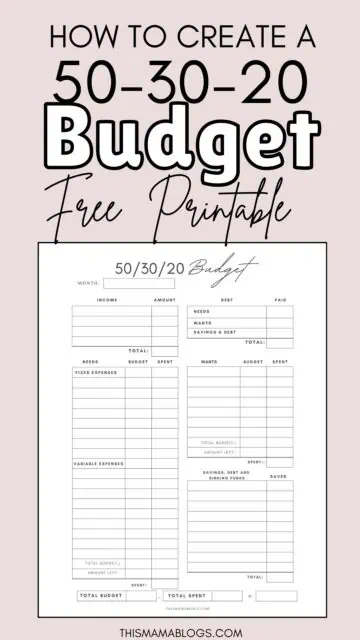

To get started, all you need is a pen and a piece of paper. If you’re feeling fancy, you can use my budget printable to make things even easier. This way, you can see exactly where your money is going and adjust as needed.

Ready to take control of your finances? Here’s how I use the 50/30/20 rule to create a budget.

1. Calculate your after-tax income.

This is the money you take home after taxes and other deductions. This includes your salary, side hustles, or any other sources of income.

If you're a freelancer, budgeting can be a bit more complex since you need to account for business expenses.

For instance, our mortgage for our new home in the Philippines—where we relocated in 2022 to retire—costs $1,254 per month. However, because I work from home, I can deduct the mortgage interest from my US business taxes. After factoring in this deduction, our actual monthly payment for the house is $851. So in this step, I figure out not only my estimate taxes but business deductions as well.

If you’re an employee with a regular paycheck, it’s pretty straightforward – just look at your pay slip to see how much you are bringing in each month. Make sure to add back in any deductions that are automatically taken out.

2. Figure out your needs.

This is the 50% part of the rule. Your essential expenses like rent, utilities, groceries, and transportation should all fall under this category.

Take a look at your bank statements or bills to see how much you are spending in these areas each month.

Once you've taken care of all your essential needs, you can start thinking about your wants. Remember, your budget for needs isn't set in stone—you can always make adjustments as your situation changes or as you find ways to optimize your spending.

In our updated budget for living here in the Philippines, our expenses have increased slightly due to the mortgages for our new car and home. However, we've also seen some savings, as our utility costs have decreased compared to what we were paying in Puerto Rico. I'm also mindful that in three years, we’ll no longer have car payments since the car will be fully paid off. This just shows how a budget can evolve, even from month to month, as your financial situation changes.

To illustrate this post, I’ve created a sample budget for average income.

2. Set aside for wants.

Next is the 30% portion of your budget, which is reserved for all your fun stuff. This is your chance to treat yourself—whether it’s dining out, shopping, catching a movie, or enjoying any activity that brings you joy.

It's important to remember that these expenses should come after you’ve covered your needs, so make sure you’re prioritizing accordingly.

Expenses you might want to include in this category are dining out, travel, movies, clothing, or hobbies.

For me, 30% feels like a lot to spend on "wants" every month. Personally, I don’t always use the full amount since my "wants" vary from month to month. For example, if I allocate $100 for clothing this month, I might not set the same budget next month because we don’t buy clothes regularly. This allows for flexibility in how I manage my discretionary spending.

When I don’t spend it all, I set aside the leftover funds into sinking funds for larger expenses, like vacations or other big purchases. This way, I’m still saving while staying flexible with my budget.

3. Budget for savings and debt repayment.

We have the 20% slice of your budget, which is all about savings and debt repayment. That might seem like a lot, but it’s actually a good rule of thumb.

When we talk about savings, we’re not just talking about throwing all your money into a piggy bank and calling it a day. We’re basically talking about managing your money wisely. It is like giving your money a job to do, so that it can work for you instead of you working for it.

When it comes to saving, don’t forget about sinking funds. A sinking fund is a separate account where you put money aside for specific expenses that you know are coming up. Let’s say, you want to go on a fancy vacation next year. Every month, you put a little bit of money into this fund until your reach your goal amount. That way, when it comes time to book your flights, you already have the money set aside, and you don’t have to dip into your regular savings.

Sinking funds can be used for all sorts of things – wedding expenses, Christmas gifts, birthday parties, home remodels, school supplies, you name it. By budgeting for these expenses ahead of time, you won’t be caught off guard when those expenses come up. Read: 15 Sinking Funds Categories to Include in Your Budget

Next up, debt repayment. Whether it’s student loans, credit card debt, or a mortgage, tackling your debt is key to financial freedom. Here’s a little tip to help you out: focus on paying off the ones with high interest rates first. Debts with high interest rates can end up costing you way more in the long run if you don’t pay them quickly. Make the minimum payments on all your debts, and then put the extra money you have towards the debt with the highest interest rate.

By dedicating a portion of your income to debt repayment, you’ll be able to pay off your debts faster and save money on interest in the long run. Plus, it feels good to see those balances go down over time.

4. Monitor and adjust.

Keep an eye on your spending each month to make sure you are sticking to your plan.

Sit down with your budget, take a look at where your money is going, and see where you can make some adjustments. We all know that cutting back on needs can be tough. That is why it’s often easier to focus on trimming down your wants instead.

Figure out which ones you can scale back on to stay within that 30%. Maybe you can skip that daily Starbucks run and make your coffee at home instead. Or perhaps you can limit your online shopping sprees to once a month. Small changes like these can make a big difference in the long run.

Final Thoughts

he 50/30/20 budget rule is a simple yet effective tool to help you take control of your finances by balancing your needs, wants, and savings.

However, creating a budget is just the first step. The real challenge lies in making sure it works for you—and that you stick to it consistently.

No matter which budgeting method you choose, one thing is essential: having clear financial goals. Whether you're saving for a big purchase, paying off debt, or building an emergency fund, knowing what you want to achieve with your money is crucial. But setting goals is only half the equation. The other half is having the discipline to follow through with your budget and turn those goals into reality.

With well-defined financial goals and the discipline to stick to your plan, you’ll be on the path to financial success.

Did you enjoy this post? Bookmark this page or save this pin to Pinterest so you can easily find your way to this post later.