Budgeting can feel easier said than done, but if there's one thing I've learned through years of managing my finances, it's this: I NEED A BUDGET.

The truth is, there are many budgeting methods out there, and finding the right one often involves some trial and error. What works perfectly for one person might not suit another, making budgeting a highly personal journey.

If you're looking for a balanced and structured approach, the 30-30-30-10 budgeting rule might be exactly what you need.

Personally, I turn to this budgeting method when I want to focus more aggressively on saving and investing. However, I also recognize that some months—especially during summer vacations or the holiday season—I prefer allocating more than just 10% of my budget to fun.

In this article, I'll walk you through exactly what the 30-30-30-10 budgeting rule entails, how to implement it effectively, and how you can maximize its benefits using my free printable budget planner.

What is the 30-30-30-10 budget?

Table of Contents

The 30-30-30-10 budget is a percentage-based budget that divides your monthly income according to these percentages: 30%, 30%, 30%, and 10%.

Here’s a specific breakdown of this budget rule.

- 30% towards housing - rent, mortgage, property taxes, etc.

This budget allocates 30% solely for housing expenses, and expenses for other necessities are excluded from this percentage. This is the money you spend to put a roof over your head, whether you’re paying rent or mortgage. This also includes all the other housing-related expenses, such as utility bills, property taxes, maintenance and repairs, and homeowners' and renters’ insurance.

- 30% towards debts and essentials - debt payments, food, transportation, utilities, and insurance.

You have 30% of your income to cover other living essentials, such as food and groceries, car-related expenses (fuel, insurance, parking fees, repairs, and maintenance), healthcare costs, and childcare expenses. A portion of this allocation also goes towards minimum debt payments.

- 30% towards investments - retirement accounts, emergency funds, stocks, etc.

This percentage covers your savings and investments. Use this money to build and maintain your emergency fund, sinking fund, savings for huge purchases, retirement accounts, and other investment vehicles (businesses, stocks, bonds, etc). You can also use part of this percentage to pay high-interest debts and get out of debt faster.

- 10% fun spending - entertainment, gifting, eating out, hobbies, travel, etc.

Lastly, you have 10% of your income towards discretionary spending. This is your fun money; you can use it however you like (within limits). Use this money for travel, funding your hobbies, and entertainment.

This budget rule provides you with a sense of structure regarding where your money should be allocated. By following these percentages, you are guaranteed to cover all your basic needs and set aside money for debt payments while building long-term wealth through investments.

It makes budgeting more manageable and less stressful, allowing you to achieve your financial goals while having some money left over for enjoyable, discretionary spending.

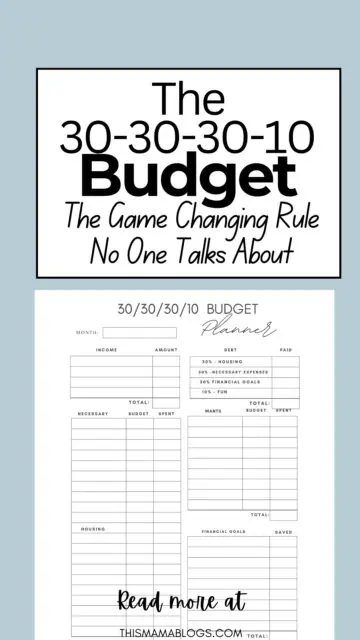

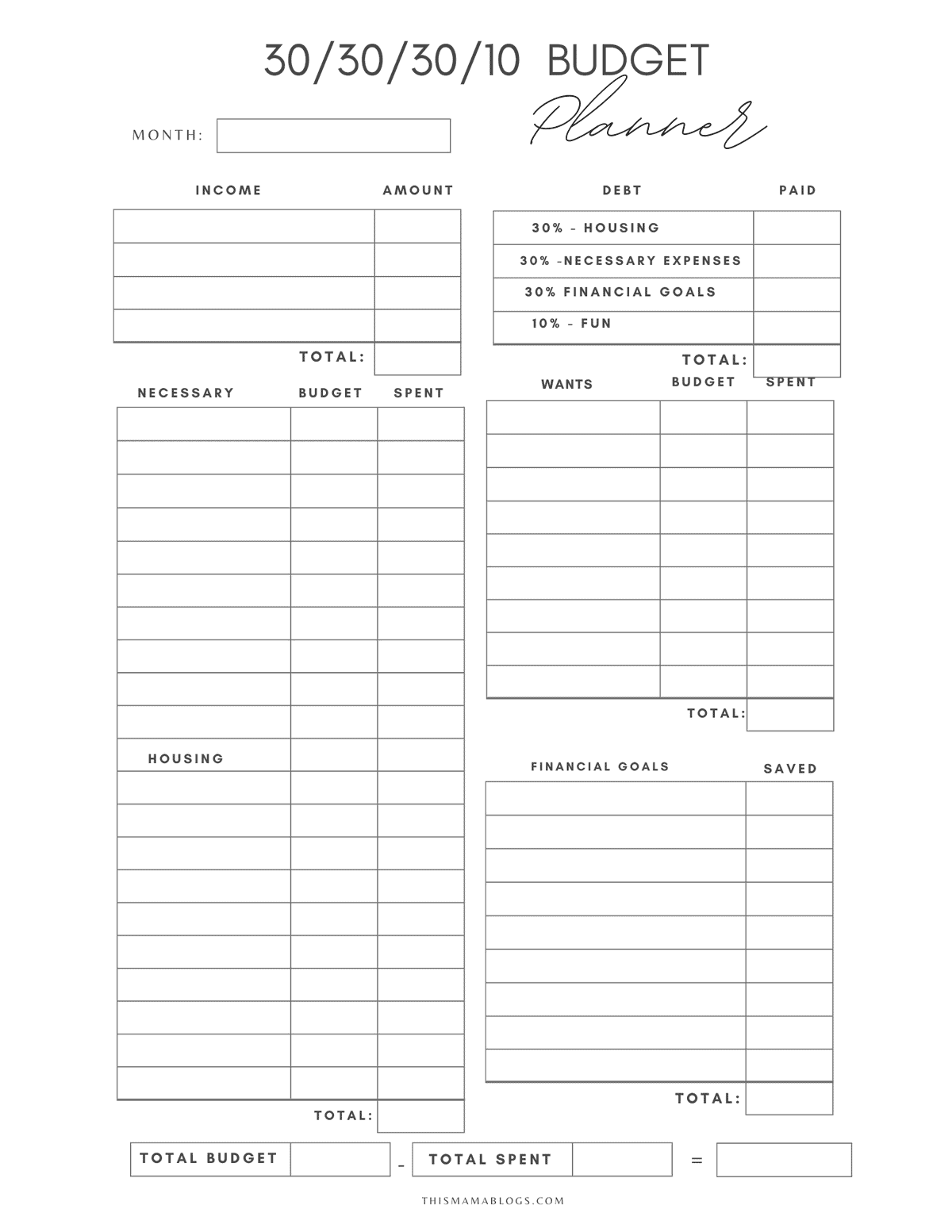

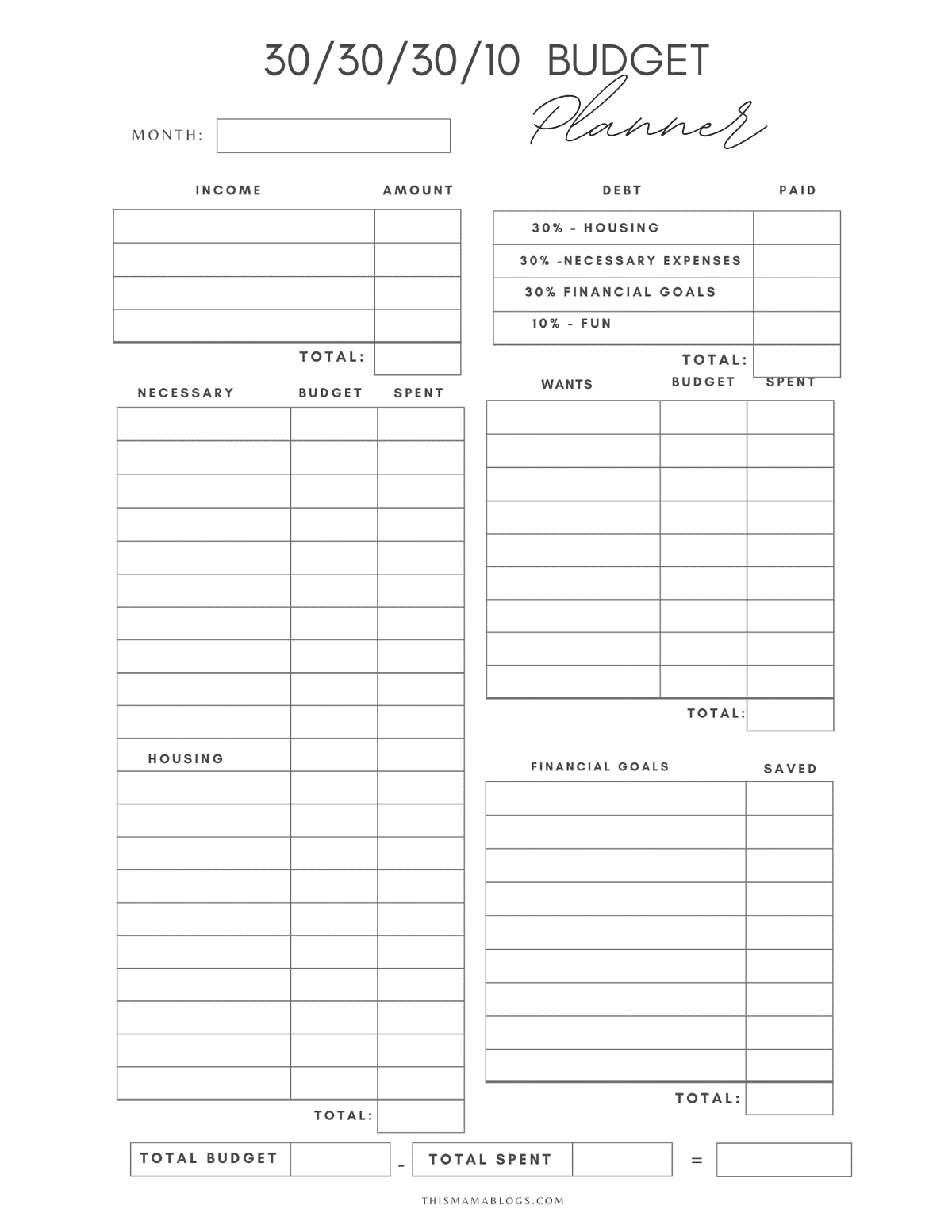

To make budgeting easy, I've created this free 30-30-30-10 Budget Planner just for you! Simply print the image below, or sign up here to get the planner delivered straight to your inbox—plus gain access to more helpful finance printables in the future!

30-30-30-10 vs 50-30-20 Budget Rule

Should you do the 30-30-30-10 rule or follow the 50-30-20 rule? While both of these budgeting methods are efficient and excellent in their own ways, they have different priorities.

Compare their differences and determine which one suits your lifestyle and financial goals best.

As you can see, the 30-30-30-10 rule emphasizes saving and investing money more aggressively. Seeing that you are to invest 30% of your income into each of these categories and another 30% towards your basic needs, it only means that you’re at a point in your life when you’re taking your financial future more seriously.

But that’s not to delimit the benefits of the 50-30-20 budget rule. With the 50-30-20 budgeting method, you’ll allocate your income this way:

- 50% towards basic needs - housing, food and groceries, utility bills, transportation, and insurance

- 30% towards wants and luxuries - shopping, entertainment, travel, hobbies, subscriptions, dining out, etc.

- 20% towards debt payment and savings - emergency fund, retirement accounts, credit card bills, and personal loans.

As you can see, with this rule, 20% of the income is allocated towards debt payment and savings, whereas it’s 30% in the 30-30-30-10 budget rule. Meanwhile, you can spend 30% of your income towards your wants, while it’s only 10% for the 30-30-30-10 budget rule.

If you want more flexible spending and enjoy your money while slowly building your savings, the 50-30-20 rule is ideal for you.

Who is the 30-30-30-10 budget for?

While both budgeting methods work, selecting one that aligns with your financial goals is crucial.

The 30-30-30-10 budget is perfect for people who want to save and invest aggressively. If you want to achieve financial independence and retire early, this rule should work because you put more toward savings and investments. As you save and invest more, the power of compound interest works in your favor, allowing you to achieve your financial goals quickly.

This rule is also ideal for people with more manageable housing expenses. If you spend less than 30% of your income on housing alone (like rent, mortgage, and property taxes), then it is easier to figure out how much you need to save each month for this specific expense.

Need to get out of debt fast? This rule works, too! This budget rule maximizes savings and investments while limiting discretionary spending to 10%, leaving you with more money for debt payments. As long as you are disciplined and committed, you should be able to pay off your debt quickly.

How to Use the 30-30-30-10 Budget Rule

Using the 30-30-30-10 Budget Rule is easy. First, write down all your income and expenses on paper. However, a more effective way to do this is to use my free budget printable, which details all the percentage allocations and the costs associated with each.

1. Get your take-home pay.

First, you must determine how much you make each month after taxes. Consider all forms of payments, whether from your day jobs, businesses, or side hustles. It’s essential to consider all your income sources and not overlook any.

2. Determine your needs.

After determining your after-tax income, it’s time to assess your needs. Remember, you have 30% of your income to allocate for these expenses, so consider how much you spend on food, transportation, insurance, and childcare. Since you are creating a monthly budget and some costs are paid quarterly or yearly, divide the total accordingly to determine the appropriate amount you need to set aside each month.

3. Allocate for savings and investments.

Another huge chunk of your income should go towards savings and investment, so go ahead and list those down, too. Decide how much you want to put towards your emergency and sinking funds, retirement accounts, college savings, etc. Also, list down all your high-interest debts and debts you’re paying more than the minimum, and take the payments from this allocation.

4. Budget for fun.

It can be frustrating to only budget for savings and investments, so consider setting aside 10% of your income as your fun money. This is the portion you spend to enjoy your hard work and have a semblance of work-life balance. You can spend time dining out, going to the movies and other fun events, spending time on your hobbies, shopping, and traveling, etc.

Tip: Be consistent but flexible. Consistently save money for your goals, but also be open to changes. For example, your budget might look different from when you were single than when you get married or have kids. Moving to a new location can impact your housing costs. Sometimes you might find that you’re not spending as much on specific categories and a lot more on others.

If you have some money left from specific categories, set that aside for future use or other specific goals. This ensures that you save monthly, pay all the bills, and have fun.

5. Monitor and adjust

As I said, our expenses and goals can evolve, and while it’s good to have and follow a budget, no budget is ever set in stone. This is where flexibility comes in. As your life and situation change, so does your budget; therefore, it’s essential to monitor and adjust it accordingly.

It’s good practice to track your expenses regularly and identify areas where you may be overspending. To reach your goals faster, trim whenever necessary and wherever feasible.

Sample Budget

Want to see the 30-30-30-10 budget rule in action? Consider these sample budgets for average and low-income earners. Remember to use my free printable when creating your budget.

Average income

According to Salary Shield, the average monthly income in the US per month is $5000.

Using the 30-30-30-10 budget rule, a monthly budget could look like.

- 30% - HOUSING ($1500) - Spend only up to this amount to cover your housing costs, which include rent/mortgage, utility bills, home insurance, and taxes.

- 30 % - DEBTS AND OTHER NECESSITIES ($1500) - You have another $1500 to spend on food, groceries, gas, childcare expenses, health insurance, and minimum debt payments.

- 30% - SAVINGS INVESTMENTS ($1500) - Use this money to save for long-term financial goals, build your emergency fund, and make investments. This is the money you save and invest for your future.

- 10 % - FUN MONEY ($500) - This is your budget for discretionary spending. Use this for buying gifts, dining out, hobbies, travel, and other things you enjoy for a happier life.

Note:

Break down each category according to your needs and goals. A larger family would spend more on food and groceries than a smaller one. The same can be said for families with more than one car, multiple children, or family members who require frequent medical attention.

Don't forget to download the helpful image below! You can easily print it out or simply sign up using the form below to have the planner delivered directly to your inbox. As a bonus, you'll also gain access to even more useful financial printables in the future!

Tip: Save this image to Pinterest or bookmark this page, so you can quickly return to it whenever you need it!

Low Income

Low income in the US can vary depending on the location and household size. You can be considered a low-income household if you earn around $ 2,500 per month for a family of four ($30,000 per year or less).

Don’t worry if you’re a low-income household and want to use the 30-30-30-10 budget rule. Here’s a sample breakdown to follow:

- 30% - HOUSING - $750

- 30% - DEBTS AND NECESSITIES - $750

- 30% - SAVINGS AND INVESTMENTS - $750

- 10% - FUN MONEY - $250

This budget ensures that you cover your basic expenses, save and invest your money, and pay down debt, while also leaving some funds for fun and miscellaneous spending. Adjust slightly if you feel like specific categories are too tight or do not apply to you. What’s important is that you stick to the budget to the best of your ability.

Final Thoughts

If you want to manage your expenses efficiently and be aggressive about saving and investing your money, the 30-30-30-10 budget rule is an excellent fit for you. Following this budget ensures that you have all the basics covered, allowing you to save consistently, while still having some money left over for the things you want and enjoy.

Remember that we are on unique financial journeys, so don’t compare your progress with others. Instead, consider your progress and adjust your budget accordingly to reflect your life changes and personal goals. It is your life, so you want to be intentional with your financial choices and decisions.

Bookmark this article if you want to use the 30-30-30-10, and don’t forget to download my free printable to make budgeting a lot easier!