Do you ever feel like no matter how hard you try to stick to a budget, you still end up overspending? Maybe it’s those sneaky impulse buys at the checkout counter or those last-minute coffee hangouts with friends. Before you know it, the month is over, and you’re left wondering, Where did all my money go?

Trust me, you’re not alone—I’ve been there too! It’s frustrating and even a little discouraging when your money doesn’t stretch as far as you’d like. But here’s the good news: there’s a way to get back in control without feeling deprived.

Have you heard of zero-based budgeting? It’s a game-changing approach that can help you take charge of every single dollar you earn. With this method, you’ll assign every dollar a job, from covering everyday things like your morning coffee to tackling bigger expenses like your mortgage and insurance.

Zero-based budgeting has been a lifesaver for me, and it’s especially helpful if you tend to overspend or feel like your money just disappears. While this budgeting strategy was originally used by companies, it’s now a favorite among families and individuals who want a clear picture of their finances.

If this sounds like something you’d like to try but you’re not sure where to start, don’t worry—I’ve got you! Let me walk you through a step-by-step guide to creating your very own zero-based budget.

But First, What is Zero-Based Budgeting?

Table of Contents

Zero-based budgeting is a method where your income minus your expenses equals zero. At first, this might sound like you’re not saving any money, but that’s not true. In fact, this approach ensures that savings, debt payments, and other financial goals are all factored into your budget.

Instead of spending money as it comes in, zero-based budgeting requires you to assign every single dollar of your income a specific purpose. You start by adding up all your expenses—big and small—and organizing them into categories that make sense for your lifestyle. For example, you might create categories for groceries, rent, utilities, transportation, and even discretionary spending, like saving for a specific goal. It’s important to be thorough and take a close look at all your expenses to ensure nothing is overlooked.

Here’s an example: Let’s say you earn $3,000 a month. With zero-based budgeting, you would allocate that $3,000 across your expense categories until every dollar has a purpose. The goal is to have your income and expenses perfectly balanced, with no extra money left unaccounted for.

The beauty of a zero-based budget is that it can be adjusted month to month or even more frequently to reflect changes in your income or expenses. To successfully stick to this budget, you must diligently track your spending to ensure you don’t spend more than you have allocated.

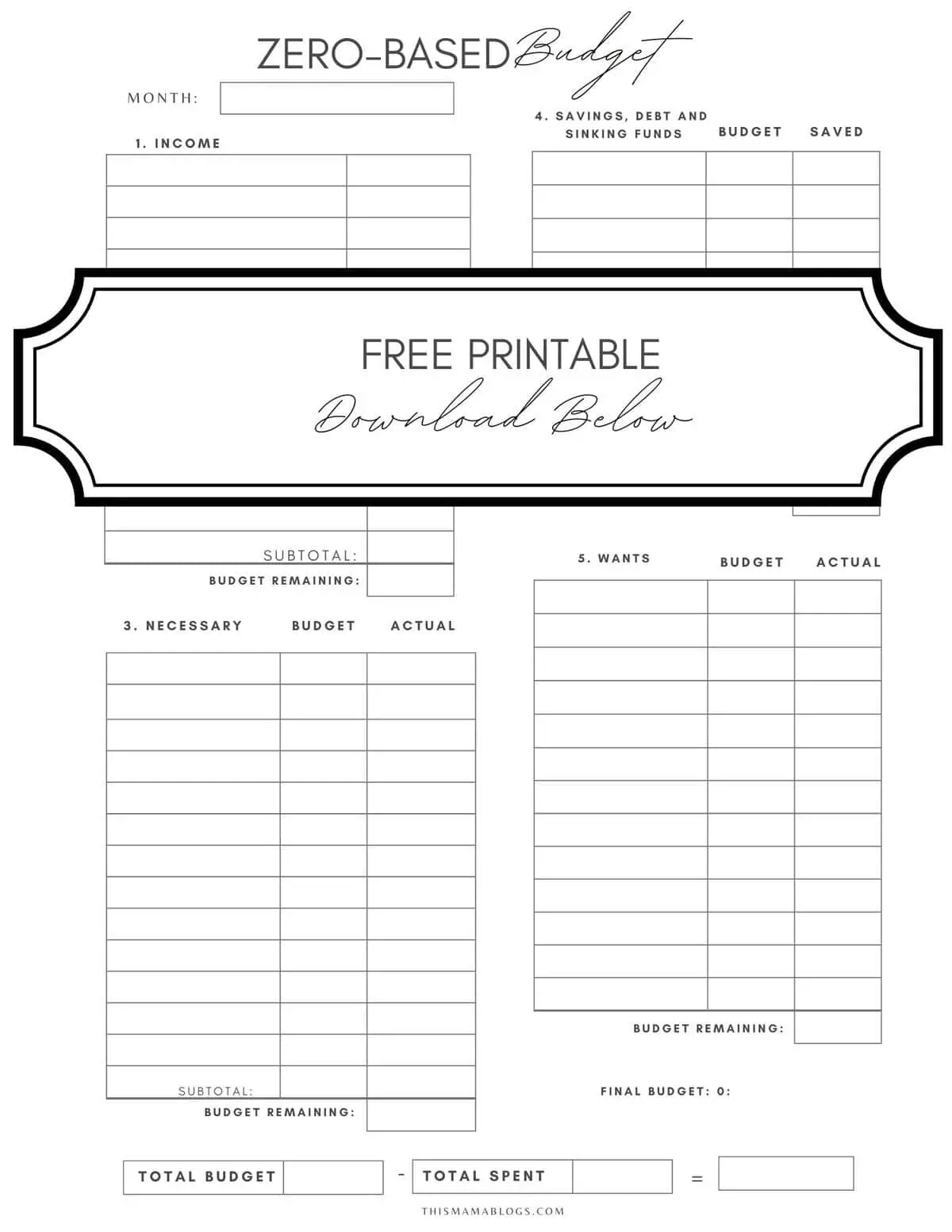

Free Zero-Based Budget Printable

Ready to take control of your finances? I’ve created a free zero-based budget printable to guide you step-by-step in building your own budget! Download it, print it, and follow the simple process from Step 1 to Step 5.

How to Create a Zero-Based Budget

With your zero-based budget worksheet in hand, let’s walk through the process of creating a budget that ensures every dollar has a purpose.

Follow these easy steps and start managing your money like a pro!

- Calculate your monthly income.

Your income isn’t just your regular salary—it includes all the money you earn from various sources.

If your income fluctuates from month to month, as mine often does in my work as a blogger, reviewing your income records from the past 12 months is an excellent starting point. If you haven’t been keeping track, now is the time to create a system for logging your earnings regularly.

When I started freelancing, I used a simple spreadsheet to log each payment I received. I included the date, client name, amount, and payment method. Over time, this gave me a clear picture of my earnings.

Action Step: Complete item #1 on your budget worksheet.

- Figure out your income after taxes.

Before diving into your expenses, it’s essential to calculate your after-tax income—the amount you actually take home after taxes and deductions.

If you receive a fixed salary with regular deductions, this step is straightforward. For those paid weekly, base your budget on four weeks of income. However, if your income fluctuates and taxes aren’t automatically withheld, the process can be a bit more complex. In this case, calculate your after-tax income and use the lowest expected amount for the month as the foundation of your budget. This approach ensures your budget remains realistic and manageable, even during lean months.

For my business, I rely on a separate spreadsheet that my accountant provided to record all my business expenses. This tool helps me see exactly how much I spend to keep my business running and, more importantly, how much of my income will remain after taxes.

As a freelancer, I make it a priority to set aside 15–20% of my monthly earnings for taxes. This approach ensures I’m prepared when tax season rolls around and helps me avoid the stress of scrambling to gather funds at the last minute. By consistently saving for taxes, I can focus on growing my business while staying on top of my financial responsibilities.

Action Step: Complete item #2 on your budget worksheet.

- List your expenses.

Now that you have a clear understanding of your income, it’s time to dive into the details of where your money is going.

Action Step: Grab a pen and paper, and write down all your expenses.

Start by pulling out your bank statements and giving them a careful review to see how much you typically spend each month for your home. Begin with your regular monthly bills—the ones you know will show up like clockwork. These include essentials like rent or mortgage payments, utilities, groceries, phone bills, and transportation. These are the core expenses that form the foundation of your budget.

Next, don’t forget about those irregular or seasonal expenses that can sneak up on you throughout the year. These might include birthday gifts, doctor’s appointments, home maintenance, or holiday expenses. Factoring these in ahead of time will help you avoid being caught off guard when they come up.

Finally, take a close look at the little indulgences that can add up over time. Whether it’s a late-night online shopping spree, a fancy dinner out with friends, or those quick coffee runs, these “guilty pleasures” need to be accounted for too. Remember, every expense counts—big or small—so be thorough when categorizing your spending.

By painting an honest and complete picture of your expenses, you’ll be better prepared to create a budget that truly works for you.

- Categorize your expenses.

Start by breaking down your expenses into bigger categories like housing, transportation, groceries, and entertainment. Once you have these larger categories in place, you can then break them down into more specific subcategories like rent, utilities, gas, dining out and streaming services.

If you are unsure of how to categorize your expenses, here are some common categories that you can use as a guide.

Housing

- Mortgage or rent

- Property taxes

- Homeowner’s or renter’s insurance

- Utilities (electricity, water, gas)

- Internet and cable

- Maintenance and repairs

Transportation

- Car Payment

- Gas and fuel

- Car insurance

- Public transit

- Maintenance and repairs

- Parking and tolls

Food and Groceries

- Groceries

- Dining out

- Takeout and delivery

Health and Wellness

- Health insurance

- Doctor visits and medical expenses

- Fitness (gym memberships, sports)

Debt Repayment

- Student loans

- Credit card payments

- Personal loans

Insurance

- Life Insurance

- Health Insurance premiums

- Car insurance

Childcare and Education

- Daycare or babysitter costs

- College savings (529 plan)

Personal Spending

- Clothing and accessories

- Hobbies and entertainment

Utilities and Household Expenses

- Electricity, water, gas

- Internet and cable

Charitable Donations and Gifts

- Charitable donations

- Gifts for holidays and special occasions

Miscellaneous

- Pet expenses (food, grooming, vet bills)

- Unexpected expenses ( appliance repairs, etc.)

While it is important to be detailed in your budget, it is crucial not to overcomplicate things by creating too many categories that may confuse you. Keep your budget simple and easy to understand so that you can stay on track with your financial goals.

- Decide how much to spend on each category.

Take a look at how much money you typically spend in different categories each month.

When it comes to certain expenses, like bills, there’s not much flexibility. These are fixed amounts that you can’t really adjust. But then there are other categories, like savings, where you have a bit more leeway. Depending on how much money you have coming in, you can adjust how much you’re putting away each month. Maybe some months you have extra cash to spare, so you can bump up your savings. Other months might be tighter, so you need to scale back a bit.

The first time I tried zero-based budgeting, I failed because I set my savings goals too high and forgot to factor in other essential expenses like house maintenance. Instead of diving right into saving, start by tackling your bills and other important expenses. This way, you’ll have a better idea of what you can realistically save each month without sacrificing your needs. The key here is to find a balance that works for you.

Action Step: Complete item #3, #4 and #5 on your budget worksheet.

- Subtract your total expenses from your total income until it equals zero.

Subtract all your expenses from your total income. Sounds easy enough, right? But here is where it gets a little tricky – you’re going to tweak your budget until all categories have a designated amount, and your income minus expenses equals zero.

One thing to keep in mind is that you might have to prioritize certain categories over others. Bills and debt repayment, for example, should probably come before discretionary spending. It’s all about making sure you’re covering the essentials before splurging on extras.

Don’t worry if you don’t get it right the first time. You might need to do a bit of trial and error to figure out what works best for you.

- Track your expenses and adjust them as necessary.

Keep a close eye on everything you spend money on, from groceries to gas to that morning coffee you can’t just live without. If you find yourself overspending in one area, simply cover the difference by moving money from another category.

Let’s say you splurged on a fancy dinner and ended up spending $20 more than you planned in the dining out category. Don’t panic! Just take $20 from another category, like entertainment or clothing, to make up for it. This way, you’ll still end the month with a balanced budget.

Examples of A Zero-Based Budget

Let’s explore two examples to see how a zero-based budget can work in different financial situations.

- Example 1: Martha’s Zero-Based Budget

Martha, a retail sales associate, earns $3,000 a month and decided to create a zero-based budget to take better control of her finances.

When Martha first set up her budget, she listed all her expenses and allocated specific amounts to each category, ensuring the total equaled $3,000—leaving no unassigned dollars. However, upon reviewing her budget, she realized she had overlooked an important category: an emergency fund.

Understanding the importance of having a safety net for unexpected expenses, Martha revisited her budget. After reviewing her spending habits, she noticed she was spending too much on entertainment and dining out. To prioritize her emergency fund, she decided to reallocate $150 from this category to start building her financial cushion.

Here’s how Martha’s adjusted budget looks:

- Rent - $400

- Utilities - $280

- Groceries - $400

- Transportation - $130

- Loans - $150

- Insurances - $120

- Clothing - $80

- Home / home maintenance - $200

- Health - $110

- Eating and Dining Out - $150

- Gym - $50

- Gifts - $90

- Pet - $50

- Travel - $110

- Emergency - $150

- Savings - $510

Total Expenses $3,000

$3,000 (Income) - $3,000 (Expenses) = $0

- Example 2 : John and Melissa's Zero-Based Budget

For a two-income family, the first step is to combine both incomes. Let’s take John and Melissa’s budget as an example.

John earns $4,000 a month, and Melissa earns $2,000, giving them a total monthly income of $6,000. They began by listing all their expenses and assigning a specific amount to each category. After totaling everything, their expenses came to $5,500, leaving them with a $500 surplus.

Instead of spending the extra money on non-essentials or letting it sit idle in a savings account, John and Melissa made a strategic decision—they allocated the $500 toward paying off their debt. This strategic decision helps them reduce high-interest charges and make progress toward financial freedom.

This proactive approach not only helps them avoid high-interest charges but also brings them closer to achieving financial freedom and greater flexibility in their future budgeting.

- Housing - $1200

- Utilities - $450

- Food and Groceries - $600

- Childcare - $700

- Car - $300

- Eating out - $200

- Insurances (Car and Health) - $400

- Transportation - $150

- Health - $200

- Entertainment - $150

- Giving - $80

- Sinking Funds ( Birthdays, Christmas, Travel ) - $400

- Emergency Fund - $300

- Savings - $370

- Debt Repayment - $500

Total Expenses $6,000

Income $6,000

- Expenses $6,000

= $0

Who Does a Zero-Based Budget Work Best For?

There isn’t one budget that fits everyone perfectly. However, there are certain people who can really benefit from using a zero-based budget.

- Enthusiastic spenders

Enthusiastic spenders are people who love to shop and tend to go overboard with their spending at times. If this sounds like you, then a zero-based budget might be just what you need to get your finances back on track. By setting strict limits on your spending in each category, you can avoid unnecessary purchases and make sure you’re putting money towards the things that matter most to you.

- Those looking to save for a big purchase

Instead of just putting money aside whenever you can, a zero-based budget gives you a clear plan to follow. Let’s say you want to save up $5,000 for a down payment on a new car. With this approach, you can decide to save $250 each month towards your goal. This way, you know exactly how long it will take you to reach $5,000 and can adjust your budget accordingly if needed.

- Those with a smaller income

When you have a smaller income, it can be easy to feel like you don’t have enough money to go around. A zero-based budget can help you prioritize your spending and make the most out of every dollar you have.

Pros and Cons of a Zero-Based Budget

Let’s take a closer look at the pros and cons so you can decide if it’s the right fit for you.

Pros

- It offers flexibility.

You get to decide how much to allocate to different expenses based on your own priorities and needs. This means that you can customize your budget to fit your unique financial situation.

- It encourages mindful spending.

No more mindlessly tossing money around on whatever catches your eye. With a zero-based budget, you have to be intentional about every dollar you spend. You have to cut out all the things that don’t matter to you and focus on what really does.

- It helps avoid unexpected expenses.

By setting aside a little bit of money each month for those irregular expenses, you’re able to plan ahead and allocate your money in a way that won’t leave you scrambling when those surprised bills come up.

Cons

- It can feel a bit restrictive.

You have to carefully look at every single expense and set strict limits on your spending. This can make it feel like there’s not much leeway in your finances.

- It is time-consuming.

With a zero-based budget, you need to keep a close eye on where every single dollar goes, from your morning coffee to your monthly bills. It requires more time and effort upfront compared to other budgeting methods.

Final Thoughts

When it comes to budgeting, there is no one-size-fits-all approach that works for everyone. However, the best budget is the one that you can realistically stick to over time that helps you stay on track financially.

Don’t be afraid to experiment with different approaches and see what best fits your situation. So, if you’re looking for a place to start, why not give the zero-based budget a try? Who knows, it may just be the framework you need to finally get your finances in order and make them work for you.